For the longest time, Global Capability Centers (GCCs) were seen as instruments of scale—efficient, process-driven, and largely tied to enterprise operations. Private equity firms, by contrast, operated as orchestrators—lean teams relying on external consultants, portfolio leadership, and fragmented data flows to drive value.

That model is beginning to crack.

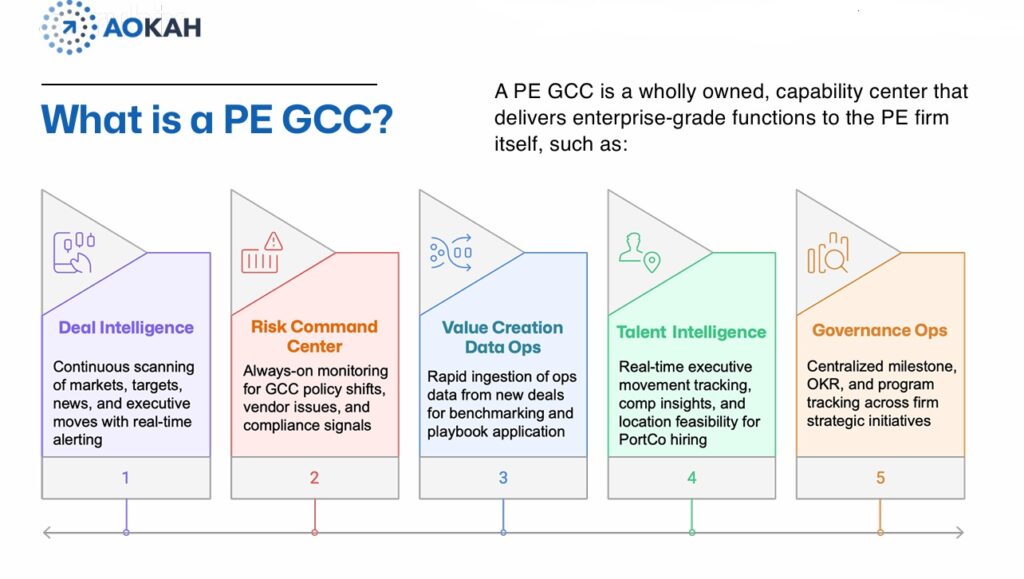

What we’re witnessing now is not just the rise of another GCC variant, but a structural shift in how private equity firms are choosing to operate. The question is no longer whether portfolio companies should build GCCs. It’s whether the PE firm itself can afford not to have one.

From Episodic Insight to Continuous Intelligence

At a fundamental level, the nature of private equity has changed. Deal cycles are compressing. Due diligence windows are shrinking. Value creation expectations from LPs are becoming sharper and more transparent. Yet, most PE firms still rely on episodic intelligence—consulting reports, static dashboards, and siloed insights that arrive too late or lack continuity.

A PE-owned GCC flips this model. It acts as a permanent intelligence layer—continuously ingesting signals across markets, talent, regulatory environments, and portfolio performance. Instead of reacting to information, firms begin to operate with forward visibility.

The Power of Repeatability in Value Creation

From a GCC Pulse lens, the real story here is not efficiency—it’s repeatability.

Private equity has always been about pattern recognition: identifying what works, scaling it across assets, and exiting at the right moment. But without a centralized capability layer, these patterns often remain trapped within individual deals or operating partners.

A GCC institutionalizes this knowledge. It captures playbooks, benchmarks performance in real time, and standardizes execution across the portfolio—without diluting the independence of individual companies. More importantly, it creates a feedback loop where every deal makes the next one smarter.

Owning Intelligence as a Competitive Moat

There’s a deeper implication unfolding. As AI becomes central to investment decision-making, the ownership of data and intelligence is fast becoming a competitive moat.

Firms that build internal capability hubs will not just move faster—they will think differently. They will rely less on external validation and more on proprietary insight engines that continuously refine decision-making.

This article is based on insights from a recent whitepaper by Aokah, titled “Why Private Equity Firms Need to Build a Global Capability Center,” which frames the PE GCC as a strategic control layer rather than a cost construct.

And that’s where the divergence begins.

The next generation of PE firms will not be defined solely by capital deployment or network strength. They will be defined by their ability to build and operationalize intelligence at scale.

In that context, a GCC is no longer optional. It is infrastructure.

Not for cost. Not for optics. But for control, continuity, and compounded advantage.