We are witnessing a profound structural strain on one of the most vital acronyms in the global technology and services landscape: the GCC, or Global Capability Centre.

What began as a precise architectural term is devolving into generic corporate jargon. Domestic retail banks expanding branch networks, Indian conglomerates scaling regional operations, and traditional IT service firms rebranding legacy delivery centers are all co-opting the GCC label.

This is not a pedantic debate over semantics. Dilution carries immediate consequences for talent positioning, policy precision, and India’s standing as the innovation capital of the world. When every local delivery office claims to be a global strategic hub, the term loses its integrity.

And when everyone is a GCC, no one is.

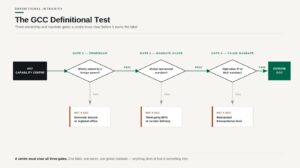

The Structural DNA: Defining the Architecture

To understand why this boundary erosion is dangerous, we must return to Grund norm. A GCC is defined by a specific, owned, and integrated capability architecture. It is an extension of a multinational corporation (MNC) headquartered outside the host country, designed to own and execute critical enterprise workflows globally.

The “Global” qualifier in the acronym is structural, not aspirational. It demands a specific operational DNA:

- Owned Governance: a wholly-owned subsidiary mirroring the parent’s culture and roadmap, not a vendor relationship.

- Multinational Scope: an architecture built to serve worldwide operations and drive global strategy.

- High-Value Mandate: a center running R&D, product engineering, and data science, not basic transactional support.

This baseline is anchored by major institutions. Karnataka’s GCC policy defines these centers as fully owned hubs by foreign-headquartered MNCs leveraging India’s talent for worldwide operational efficiency. nasscom defines a GCC as a centralized unit within a multinational providing high-value services globally. HFS Research positions the modern GCC as an enterprise-owned capability engine with direct governance over AI, analytics, and digital transformation, separate from traditional outsourcing.

When a domestic entity opens an office to serve local customers, that is domestic growth. It is a vital economic driver, but it is not a GCC.

The Friction Points: Talent, Policy, and Tax

Allowing these boundaries to blur triggers friction across three pillars.

Talent market disorientation: engineers need to know if they are joining a team with true product ownership or a rebranded domestic execution desk, and diluted terminology distorts career expectations.

Policy and resource dilution: governments build incentive frameworks to anchor high-value FDI, and when local expansions appropriate the label, the underlying economic data turns muddy, misdirecting state resources.

Regulatory and tax instability: the current wave of GST scrutiny over intermediary classification shows why structural clarity is a regulatory shield, not a marketing asset. True GCCs carry a clear, defensible transfer pricing and tax profile; indiscriminate use of the term generates compliance noise that harms legitimate hubs.

The Sovereign Benchmark: The Need for Definitional Discipline

Other economic capitals guard this kind of boundary fiercely. Singapore’s Economic Development Board enforces precise headcount, spend, and decision-authority criteria before granting Regional Headquarters status. Ireland does not let every foreign subsidiary call itself a European Centre of Excellence. They understand that structural definitions dictate macroeconomic positioning.

India’s story has shifted from labour arbitrage to value and capability arbitrage, and the country has become the default innovation engine for the Fortune 500. That positioning is fragile if the market lets the GCC definition dissolve into a catch-all for any office with an internet connection.

Preserving India’s Innovation Capital

This is not a case for rigid bureaucratic policing. There are legitimate nuances, such as an Indian multinational building a specialized capability center in a Tier-2 city to run its South Asian operations.

But the word Global must retain its weight: a foreign-headquartered parent, an international scope, and a mandate built beyond domestic borders.

The premier centers in Bengaluru, Hyderabad, Pune, and NCR are no longer backend cost centers. They are the digital brains and primary IP generators for the world’s largest enterprises, and that evolution deserves institutional definitions that protect it.

If India wants to hold its position as the undisputed innovation and GCC capital of the world, we must guard our terminology with the same rigor we apply to our engineering.

Strong piece, Yashasvi — the “owned governance” pillar is the right anchor, but it raises a few practical questions worth debating. If your 100% ownership model is true most of so called GCC will not fall in GCC bucket 🙂

1. Where does a BOT (build-operate-transfer) center sit during the transition window — say, Hy-Vee India case? Not a GCC pre-transfer, but is it one the day ownership flips, or only once operational control catches up?

2. Minority/JV stakes – Many “GCCs” in India are 51-74% owned joint ventures rather than wholly-owned subsidiaries (common in regulated sectors like insurance/BFSI). Does “wholly-owned subsidiary” as the bar exclude these, or is there a threshold?

3. Governance vs. legal ownership: A center can be 100% legally owned by the parent but run largely on a staffing/BOT vendor’s HR and delivery layer with the MNC only owning IP and roadmap. Is that “owned governance,” or does operational control matter more than the cap table?

4. Karnataka’s policy, nasscom, and HFS Research don’t fully converge on thresholds — so practically, whose definition should tax/policy bodies default to when they conflict?

Curious how you’d draw these lines in practice, not just in principle.